If you’ve reached your 50s, you may find that you’re falling short of your retirement goals. Yet you may also have a little more disposable income than you used to. The federal government realizes all this, too, and that’s why people age 50 and older can contribute substantially more to their 401(k) or 403(b) plan than younger ones can. Here are some basics on catch-up contributions and how to put them to work.

The IRS sets limits on how much people can save for retirement in different types of retirement plans. They also review the limits every year to be sure they’re keeping up with inflation. The annual limit on traditional (pretax) and Roth (after-tax) contributions will be $20,500 in 2022, which is $1,000 higher than in 2021, but when you add in the additional $6,500 contribution available to older workers in 2022—known as the catch-up contribution—the total yearly limit rises to $27,000.

This can create substantial headroom for preretirees committed to helping build their retirement assets in the years ahead.

It’s convenient to make catch-up contributions

If you already participate in your workplace retirement plan, all you need to do is increase your contribution amount online or by phone, the way you always have. The catch-up allowance simply increases your own personal contribution limit. Otherwise, there’s no difference at all between regular and catch-up contributions.

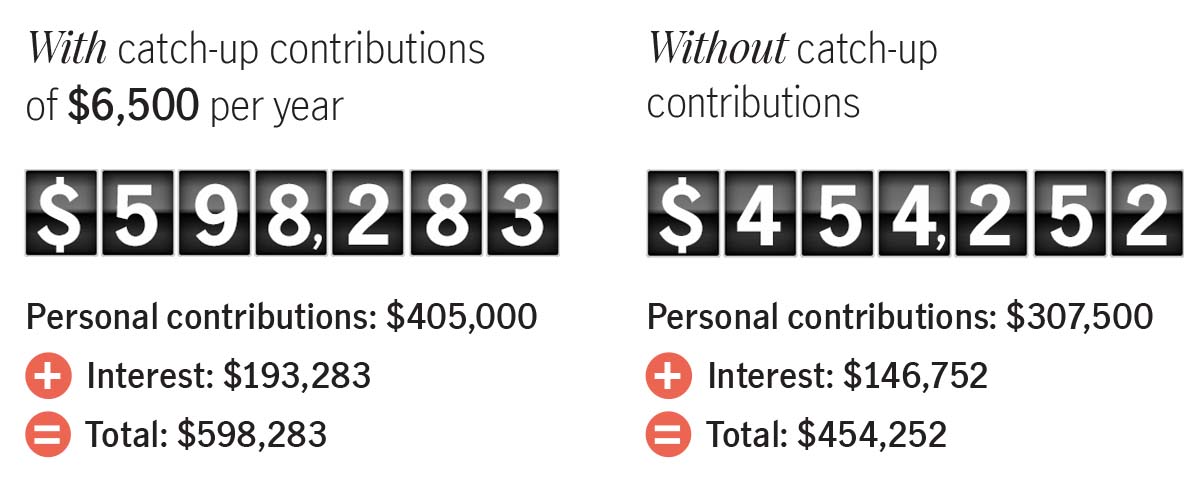

How big a difference can saving up to the 2022 maximum retirement contribution make?

Over time, the benefits of maxing out your regular contributions and taking advantage of your catch-up opportunity can be substantial.

The following hypothetical examples assumes that you save from ages 50 through 65 at the total 2022 allowable maximums—with or without catch-up contributions.

The potential impact of maxing out your annual contributions—including catch up

This hypothetical example is for illustrative purposes only. There is no guarantee that the results shown will be achieved or maintained over any time period.

As these numbers show, taking advantage of catch-up contributions could net you an extra $100,000 or more in retirement assets, due to the additional money you’ll put away and the opportunity for compounded growth.

Even more remarkable, this doesn’t include any balance you might have built before age 50.

Rules you should know about catch-up contributions

As with regular plan contributions, the IRS reviews and can make cost-of-living adjustments to catch-up limits every year.

Catch-up contributions are only available if your plan allows, although most of them do.

An alternative to consider

As you move into your 50s and 60s, you may find yourself with additional cash on hand that you didn’t have in earlier years. Often, this extra money ends up in a low-interest savings account—or in taxable investments.

Steering a few thousand dollars more per year into your workplace savings plan can provide both attractive tax advantages and the potential for growth. Also, if you decide to do some formal retirement income planning, catch-up contributions are a convenient way to help close any gap between your expected expenses and projected cash flow.

See if you can help maximize your savings with catch-up contributions

If you’re age 50 or older—or soon will be—check to see how much more you can contribute on atax-advantaged basis. Not only could it help you catch up to your retirement goals, but, as part of a broader strategy, it could even help yousurpassthem.

As indicated, figures for the illustrations are based on assumptions as set out, and individual circumstances may vary.

The content of this document is for general information only and is believed to be accurate and reliable as of the posting date, but may be subject to change. It is not intended to provide investment, tax, plan design, or legal advice (unless otherwise indicated). Please consult your own independent advisor as to any investment, tax, or legal statements made herein.

© 2019–2022 John Hancock. All rights reserved.