401(k) Compliance Checklist: What Every Employer Needs to Know

As an employer, offering a 401(k) plan is one of the most impactful ways to support your employees' financial futures. However, managing a 401(k) plan also comes with important responsibilities, particularly when it comes to compliance. Failure to comply with regulatory requirements can lead to significant penalties, legal complications, and even damage to employee trust.

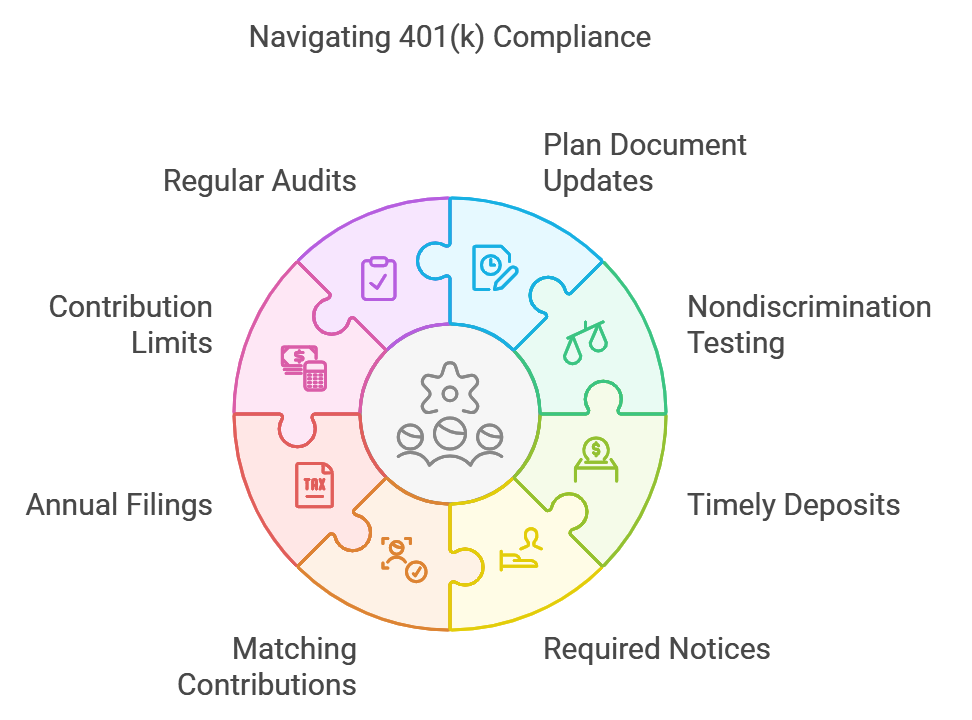

To help you navigate this complex landscape, we’ve created a 401(k) Compliance Checklist to ensure your plan remains compliant, effective, and beneficial for all participants.

1. Keep Your Plan Document Up-to-Date

Your 401(k) plan document serves as the foundation of your retirement program. It outlines the plan’s rules, eligibility requirements, contribution limits, and distribution policies.

Action Steps:

- Review your plan document annually to ensure compliance with the latest IRS and Department of Labor (DOL) regulations.

- Implement amendments as required by law or due to changes in your organization.

2. Conduct Nondiscrimination Testing

Federal regulations require 401(k) plans to undergo annual testing to ensure fairness between highly compensated employees (HCEs) and non-highly compensated employees (NHCEs). These tests include:

- ADP Test: Evaluates employee deferral rates.

- ACP Test: Examines employer matching contributions.

- Top-Heavy Test: Ensures a fair balance of plan benefits.

Pro Tip: Safe Harbor 401(k) plans automatically pass these tests if specific criteria are met.

3. Deposit Employee Contributions on Time

Employers must deposit employee contributions into the 401(k) plan as soon as administratively possible, typically within 7 business days. Delayed deposits can result in penalties and the requirement to pay lost earnings to affected employees.

4. Distribute Required Notices

Certain notices are required to keep employees informed and maintain compliance:

- Safe Harbor Notice (if applicable): Explains plan provisions.

- Summary Plan Description (SPD): Outlines plan details and participant rights.

- Blackout Period Notices: Informs employees of temporary restrictions on account activity during administrative changes.

Action Step: Develop a communication calendar to ensure timely distribution.

5. Verify Employer Matching Contributions

Employer contributions, including matching or profit-sharing amounts, must be calculated and applied accurately. This ensures fairness and avoids costly errors.

Tip: Regularly audit your payroll and contribution processes to prevent discrepancies.

6. Complete Annual Filings

401(k) plans are required to file an annual Form 5500 with the IRS and DOL. This form provides detailed information about the plan’s financial condition and compliance status.

Key Points:

- File Form 5500 by the required deadline (usually the last day of the 7th month following the plan year-end).

- Maintain accurate and thorough records for audits.

7. Stay Informed on Contribution Limits

Ensure all contributions adhere to the IRS annual limits, which are updated yearly. For 2025, the limits are:

- Employee Contributions: $23,500

- Catch-Up Contributions (age 50+): $7,500

- Catch-Up Contributions (age 60-63): $11,250

- Total Annual Contributions (employer + employee): $70,000 or $77,500 with catch-up contributions

8. Perform Regular Plan Audits

Auditing your plan regularly can help identify issues before they become compliance problems. Areas to review include:

- Payroll and contribution data accuracy.

- Plan fees and their reasonableness.

- Employee eligibility and vesting schedules

Partner with Experts for Peace of Mind

Managing a 401(k) plan can be complex, but you don’t have to do it alone. At StatonWalsh, we specialize in helping employers navigate compliance requirements while optimizing their retirement plans for both the organization and its employees.

Our Services Include:

- Plan reviews and compliance checks.

- Assistance with nondiscrimination testing.

- Support with required filings and documentation.

Take the Next Step

A compliant 401(k) plan isn’t just a regulatory requirement—it’s a way to show your employees you care about their financial well-being. With the right strategy and support, you can ensure your plan runs smoothly while avoiding unnecessary penalties or risks.

📞 Ready to simplify 401(k) compliance? Schedule a consultation with our retirement plan experts today.

🔗 Calendly